Why Indian Companies Are Betting Big on CDPs.

The question arrived quietly, midway through a quarterly business review at one of India’s largest retail conglomerates. The Chief Marketing Officer paused, looked around the room, and asked:

‘Who, exactly, is our most valuable customer?’

What followed was not an answer. It was a slow, revealing unraveling. The CRM team cited loyalty-tier rankings. E-commerce pulled up purchase frequency from the marketplace dashboard. Digital marketing referenced ROAS-weighted cohorts. Finance had its own lifetime value model. Each number was real. None agreed.

The meeting had stumbled onto the central paradox of the modern Indian enterprise – an organisation drowning in data, yet starved of insight.

“We had seventeen dashboards and still could not answer a basic question about our customer with confidence. That was the moment we understood something was fundamentally broken.” – Chief Data Officer, leading Indian FMCG company

This gap between data availability and data usability is precisely where Customer Data Platforms (CDPs) have found their moment. And across sectors from banking to beauty to quick commerce, Indian enterprises are moving fast to close it.

The Fragmentation Problem and Why India Has It Worst

The modern Indian consumer is a study in digital omnipresence. She might discover a product on Instagram Reels, research it on a marketplace, message the brand on WhatsApp, earn loyalty points via a superapp, and still close the transaction at a physical store. Each interaction leaves a data signature. In the vast majority of Indian enterprises, each of those signatures lives in a different silo.

This problem is not unique to India, but India’s version of it is particularly acute, shaped by three structural forces that compound the challenge.

A Market Too Heterogeneous to Generalise

India is not one consumer market. It is a federation of several dozen or more, differentiated by language, culture, purchasing power, and digital maturity. A campaign that converts in Coimbatore may confuse consumers in Chandigarh. A price architecture built for metros collapses in Tier 3 towns. Without data unified at the individual level, not aggregated by segment or region, personalisation remains, at best, a sophisticated guess.

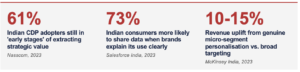

According to McKinsey’s 2023 India consumer research, brands that achieve genuine micro-segment personalisation report revenue lifts of 10-15% compared to peers relying on broad demographic targeting. In India’s fiercely competitive consumer landscape, that gap is existential.

The Omnichannel Explosion

India added over 250 million new internet users between 2019 and 2023, pushing total online reach past 900 million. This expansion was not gradual. It was compressed, turbocharged by cheap data, affordable smartphones, and a pandemic that digitised behaviours overnight.

As a result, brands must now maintain coherent relationships across channels they did not anticipate, at a pace their legacy infrastructure was never designed to support. Customers are omnichannel by default. Most enterprise data systems are still mono-channel by design.

The Privacy Inflection

India’s Digital Personal Data Protection (DPDP) Act, enacted in August 2023, marks a structural turning point. While enforcement timelines continue to be clarified, the direction is unambiguous – third-party data is becoming legally and commercially riskier to acquire, and customer consent is becoming a non-negotiable foundation for any data strategy.

In this environment, first-party data collected directly, transparently, and consensually is no longer merely a compliance advantage. It is an emerging competitive moat.

What the DPDP Act Means for Marketers

Under India’s Digital Personal Data Protection Act, 2023, organisations must obtain explicit, granular consent before collecting and processing personal data. Consent must be specific to the purpose and easily withdrawable. Non-compliance carries penalties of up to ₹250 crore per violation. For marketers, this makes the CDP – as a system of record for consent and first-party data – not a strategic option, but a regulatory necessity.

What a CDP Actually Does and What It Does Not

There is considerable noise in the market about what a Customer Data Platform is, much of it vendor-generated. The definition that matters strategically is straightforward:

A CDP ingests data from every touchpoint where a customer interacts with a business and resolves it into a single, persistent, updatable profile that is accessible to every function – marketing, product, sales, and service.

It is not a CRM, which manages current relationships. It is not a data warehouse, which stores historical transactions. And it is not a marketing automation tool, which executes campaigns. It is the connective tissue between all of these. It is the system that ensures every function is working from the same understanding of who the customer is.

“A CDP is to customer intelligence what electricity is to appliances – a prerequisite, not a product. The value lies entirely in what you build on top of it.”

This distinction matters because many implementations falter precisely here. Organisations invest in the platform but underinvest in the capability to use it. The technology arrives; the transformation does not. A 2023 Nasscom survey of Indian enterprises found that 61% of organisations that had deployed a CDP reported being ‘in early stages’ of extracting strategic value from it, citing talent gaps and misaligned incentives as the primary barriers.

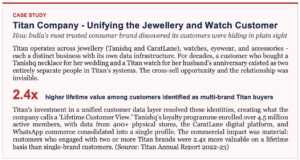

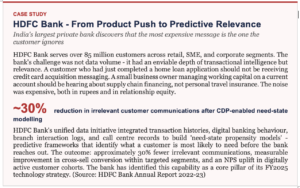

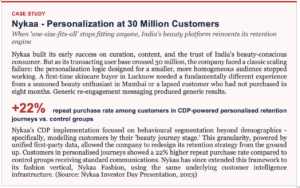

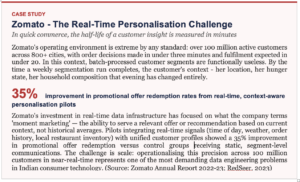

From Theory to Traction: Four Indian Enterprises Rewriting the Playbook

Across banking, retail, beauty, and consumer goods, a cohort of Indian companies has moved beyond proof-of-concept into what practitioners are calling the ‘operational phase’ of CDP maturity, where unified data is beginning to reshape strategy, not just campaign performance.

The Organisational Fault Lines CDPs Expose

Executives who have navigated a CDP implementation tend to share a consistent observation – the technology was, by some distance, the easier part. The harder work was organisational, and it exposed tensions that had long existed beneath the surface.

Data Silos Are Power Silos

In most large Indian enterprises, data silos are not technical failures. They are political ones. When the CRM is owned by sales, behavioural analytics by digital marketing, and the transactional database by finance, each team has both an incentive and an implicit mandate to protect its data territory. Integration requires not just APIs, but agreements – about ownership, accountability, and what happens when unified data tells a story that someone would prefer remained untold.

The most successful CDP implementations in India have almost universally been championed at the C-suite level. Without executive sponsorship that cuts across departmental boundaries, the platform becomes just another integration project: technically complete, strategically inert.

The Talent Gap Is Real

India produces engineering talent at an extraordinary scale. What it still lacks, at the intersection of commerce and data, is the business-technical hybrid: professionals who can sit between a marketing team and a data engineering team, translating commercial questions into analytical frameworks and data outputs back into strategic decisions.

A 2023 Deloitte India study found that 68% of enterprises identify ‘insufficient internal analytics talent’ as a primary barrier to extracting value from data investments ahead of budget constraints and technology limitations. This gap does not close through hiring alone. It requires deliberate investment in capability building: training marketing and product teams to think in data, and training data teams to think in business outcomes.

The Patience Problem

Unlike performance marketing tools that deliver measurable results within a campaign cycle, a CDP’s value is compounding and lagging. The first quarter of unified data looks, on most dashboards, not dramatically different from the last quarter of fragmented data. The difference emerges over time as models improve, as teams build interpretive confidence, and as the understanding of the customer deepens from a snapshot into a moving picture.

In organisations where marketing leaders are measured on quarterly numbers, this creates a structural tension that has derailed many otherwise sound implementations. The business case for CDPs must therefore be made not just analytically but narratively, framing the investment as infrastructure, with the patient honesty that infrastructure demands.

“The CDP did not change our results in Q1. It changed how we make decisions. By Q3, that started showing up in the numbers.” – VP Marketing, Indian D2C unicorn, Series C

Why First-Party Data Is Now a Race

If the strategic case for CDPs was compelling before 2022, the emergence of generative AI and large language models has made it urgent. AI-driven personalisation, whether in content generation, next-best-offer modelling, churn prediction, or dynamic pricing, is only as good as the data it is trained on. Organisations with unified, consented, high-quality first-party data can build AI systems that genuinely reflect their customers. Organisations working from noisy, fragmented datasets are building AI on structured guesswork.

India’s AI-in-enterprise market is projected to grow from $6.1 billion in 2023 to over $28 billion by 2028, according to Nasscom – a near five-fold expansion in five years. The organisations positioned to capture that value disproportionately will be those who built the data foundation first.

The Generative AI Dependency

Every generative AI application in marketing – personalised content at scale, conversational commerce, predictive customer service is critically dependent on the quality and completeness of underlying customer data. A CDP does not make AI possible; poor data makes it counterproductive. India’s AI investment wave and its CDP adoption curve are not parallel trends. They are the same trend, viewed from different angles.

India’s regulatory environment reinforces this dynamic. As the DPDP Act constrains the use of third-party data, organisations that have built robust first-party data assets and the platforms to activate them will find themselves with a structural advantage that is difficult and slow for competitors to replicate.

What Indian Business Leaders Should Do Now

The strategic path forward is neither uniform nor simple. But several principles have emerged consistently from the organisations executing most effectively.

Start With the Question, Not the Platform

The most common failure mode in CDP adoption is beginning with a technology selection process. The right starting point is a set of business questions that cannot currently be answered, and working backwards to identify what data infrastructure would enable them. Technology is a means. Starting with it as an end produces platforms that are well-integrated but strategically purposeless.

Treat Consent Architecture as a Competitive Asset

In the post-DPDP world, how an organisation manages customer data consent, storage, and usage is not a legal question alone. It is a trust question. Brands that build demonstrably ethical data practices are constructing a relationship asset that compounds over time. Those who treat consent as a compliance checkbox will find the regulatory floor rises faster than their systems can adapt.

Build for India’s Edge, Not India’s Average

The temptation in any large-scale data initiative is to optimise for the median customer. In a market as diverse as India, the median customer is a statistical abstraction who describes almost no one. The real commercial value lies at the edges in the micro-segments, the regional variations, the context-specific behaviours that drive actual purchase decisions. Invest in the capability to act on granularity.

Measure Differently Or Measure the Wrong Things

If CDPs are evaluated against the same metrics as campaign tools – immediate ROAS, short-term revenue uplift, next-quarter conversion rates- they will almost always disappoint. Build a measurement framework that captures leading indicators of long-term customer value – profile completeness and enrichment rates, segment migration velocity, prediction model accuracy over time, and cross-channel engagement depth. These metrics are slower but truer.

The Shift That Cannot Be Deferred

India’s most sophisticated enterprises are no longer asking whether to invest in customer data infrastructure. They are asking how quickly they can do it and whether enough of their existing data estate can be salvaged into something coherent enough to build on.

The urgency is justified. As AI reshapes the economics of personalisation, and as privacy regulation raises the cost of third-party data dependency, the gap between organisations that control their customer understanding and those that do not will widen.

But the deepest shift is not technological. It is conceptual.

For decades, Indian marketing has been structured around campaigns planned in sprints, measured in cycles, and optimised for the immediate response. CDPs enable a different model entirely – one where the customer relationship is continuous, the data is cumulative, and the engagement is genuinely contextual rather than situationally generic.

That is the shift from campaigns to customer systems, from data collection to data intelligence, from the average to the individual. The companies that make it will not simply market better. They will compete differently.

For Indian enterprises navigating scale, diversity, and compounding competitive pressure simultaneously, that shift is no longer a strategic option. It is the terrain on which the next decade of growth will be won or lost.

SOURCES & REFERENCES

- Gartner (2024). Magic Quadrant for Customer Data Platforms. Gartner Research.

- RedSeer Strategy Consultants (2023). India Digital Consumer Report 2023. RedSeer.

- IAMAI & Kantar (2023). Internet in India 2023. Internet and Mobile Association of India.

- Salesforce (2023). State of the Connected Customer — India Edition. Salesforce Research.

- McKinsey & Company (2023). The Next Frontier of Customer Engagement: AI-Enabled Personalization at Scale. McKinsey Digital.

- Nasscom (2023). AI Adoption in Indian Enterprises: Barriers and Opportunities. Nasscom Research.

- Tata Consultancy Services (2023). The Data-Driven Enterprise: Insights from 500 Indian CXOs. TCS Thought Leadership.

- Titan Company Ltd. (2023). Annual Report 2022-23. BSE India.

- HDFC Bank (2023). Annual Report 2022-23 — Technology & Digital Initiatives. HDFC Bank Investor Relations.

- Reliance Retail Ventures Ltd. (2023). Annual Report 2022-23. Reliance Industries.

- Nykaa (FSN E-Commerce Ventures Ltd.) (2023). Investor Day Presentation. Nykaa IR.

- Zomato Ltd. (2023). Annual Report 2022-23. Zomato Investor Relations.

- Ministry of Electronics & IT, Government of India (2023). Digital Personal Data Protection Act, 2023.

- Boston Consulting Group (2023). From Mass to Micro: Personalization Imperatives in Indian Consumer Markets. BCG Henderson Institute.

- Deloitte India (2023). The Analytics Talent Gap: Bridging the Distance Between Data and Decision. Deloitte Insights.

- IDC India (2023). India Customer Data Platform Market Forecast, 2023-2027. IDC.

Note: Case study figures represent outcomes reported in public company filings, investor presentations, and industry research. Specific internal metrics are attributional to source documents cited. This article has been prepared for informational and strategic discussion purposes.

Post a Comment