The Real Reason BFSI Personalization Still Feels Generic.

There is a moment that many banking customers know intimately. You log in, and the screen says –

“Good morning, Amit. Your account balance is ₹2,14,330.”

For a fleeting instant, it almost feels personal. Then the next banner offers you a home loan, the same one that has been there since January. The moment evaporates.

Banks and insurers have invested billions in personalization. So why does it still feel like a mail-merge?

This is the central paradox of personalization in Banking, Financial Services, and Insurance (BFSI) – an industry that holds more intimate data about human behavior than almost any other on earth, yet routinely delivers experiences that feel as generic as a mass-market flyer.

The problem is not a lack of investment. According to McKinsey, financial institutions have poured hundreds of billions into digital transformation over the past decade. Personalization platforms, CRM overhauls, and data lakes have proliferated.

Yet a 2023 Accenture survey found that 67% of banking customers feel the personalization they receive is “superficial” or “irrelevant.” The gap between ambition and execution has never been wider.

The reason is both structural and philosophical. Most BFSI personalization today is not really personalization at all. It is sophisticated templating, and understanding the difference is the first step toward closing the gap.

The Illusion of Personalization. When ‘Hi, Amit’ Is as Far as It Goes

Walk into any major bank’s digital product today, and you will find the hallmarks of first-generation personalization – your name on the dashboard, your most-used services surfaced to the top, perhaps a birthday message in November. These are not trivial achievements. They represent years of backend integration and UX work. But they share a fundamental limitation – they are driven by static identity, not dynamic behavior.

This is what we might call “Nominal Personalization”. The customer is recognized, but not understood. The system knows who you are; it does not know what you are doing, what you are about to need, or what would genuinely help you right now.

Compare that to what Contextual Personalization looks like in practice. A bank’s spending analysis feature should not just show you a pie chart of last month’s expenses. It notices that you have booked three international flights in 90 days and proactively surfaces its travel rewards card with a personalized ROI calculation based on your actual spend. Netflix’s recommendation engine – the gold standard most financial brands cite in internal decks but rarely emulate does not just remember what you watched. It models what you are likely to want next, based on the time of day, inferred recent mood shifts from genre switching, and what similar users chose.

The distance between “Hi, Amit” and “Your travel spending suggests you could save ₹18,000 a year with this card” is not merely cosmetic. It is the distance between recognition and relevance, and it is where the vast majority of BFSI brands are stuck.

“Personalization without intelligence is just templating and no amount of first-name tokens changes that.”

Why Most Personalization Is Rule-Based, Static, and Segment-Driven

To understand why BFSI personalization feels hollow, you need to understand how most of it is actually built. Beneath the glossy interfaces, the majority of personalization engines in financial services run on one of three architectures, and all three share the same fundamental flaw.

Rule-Based Engines

The industry workhorse. A compliance team and a marketing team sit down and define conditions – “If a customer has a savings account and balance > ₹1 lakh and age > 35, show fixed deposit banner.” These rules are legible, auditable, and easy to explain to regulators. They are also brittle. Rules cannot adapt to a context they were not written for. They cannot learn. And as any data scientist who has inherited a legacy rules engine will tell you, they metastasize over time into thickets of contradictory logic that nobody fully understands.

Segment-Driven Targeting

The next evolutionary step beyond pure rules is segmentation. Customers are grouped by age, income band, product holding, or RFM score, and each segment receives tailored messaging. This is better than one-size-fits-all, but it reintroduces the generic experience through the back door. A segment is, by definition, a generalization. “Urban millennial with home loan” is not a person. Treating 400,000 people as if they are the same individual because they share three demographic attributes is not personalization; it is mass customization with extra steps.

Static Profiles

Perhaps the most pernicious limitation. Most CRM systems capture a snapshot of who a customer was at onboarding, updated sporadically when they call the helpline or take a new product. They do not capture the customer’s financial journey in motion—a sudden spike in medical payments, a pattern of late-night small-value transactions that may signal financial stress, or the six consecutive Saturdays spent browsing home loan calculators without converting. These behavioral signals are the raw material of genuine personalization, and they are going largely uncollected or unacted upon.

The Disconnect Between Data and Action

Here is the most striking irony in financial services – banks know more about their customers’ real financial behavior than almost any other institution on earth. Every transaction is a data point. Every ATM withdrawal at 2 a.m. tells a story. Every lapsed SIP is a signal of something. It could be a change in income, a loss of confidence, or a life event.

Yet this data sits largely inert in transaction ledgers, used primarily for fraud detection and regulatory reporting. The behavioral exhaust of daily financial life is not being converted into intelligence that drives the customer experience.

Why? Three structural reasons stand in the way.

Data silos

Retail banking, credit cards, insurance, and wealth management typically run on separate core systems, with separate data warehouses. Even within a single financial group, getting a unified view of one customer’s behavior can require crossing four different technology stacks.

Regulatory caution

Compliance teams are wary of being perceived as using intimate financial data for sales purposes. The result is an overcorrection. Data that could be used to genuinely help customers (flagging potential fraud earlier, proactively offering overdraft protection before a payment bounces) sits unused because no one wants to be the person who signed off on it.

Organizational misalignment

Personalization requires the marketing team, the data science team, the product team, and the technology team to operate in close coordination, with a shared definition of what a good outcome looks like. In most large financial institutions, these teams have separate P&Ls, separate quarterly targets, and separate ideas about what the customer journey should feel like.

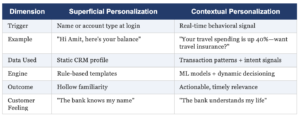

Superficial vs. Contextual Personalisation. A Framework

The table below captures the core distinction between where most BFSI brands are today and where the leaders are heading.

The Insurance Sector’s Particular Blind Spot

If banks are behind on personalization, insurers are in a different time zone. The insurance sector has historically had one of the most transactional, low-engagement customer relationships in financial services. Most policyholders interact with their insurer twice: once when they buy the policy, and once when they file a claim. Everything in between is silence.

This is a missed opportunity of staggering proportions. Insurers possess, or could possess, a remarkable breadth of behavioral data by driving patterns (telematics), health metrics (wearables), home usage data (smart home devices), and travel behavior (card transactions). Progressive Insurance’s Snapshot telematics program demonstrated years ago that real-time behavioral data could be used to price risk more accurately and reward good behavior with lower premiums – a form of personalization that is genuinely valuable to the customer.

Yet most insurers still send the same annual renewal notice to a 28-year-old who runs marathons and a 58-year-old with three chronic conditions. The policy is the unit of analysis, not the person. Until insurers shift from product-centric to life-stage-centric engagement models, they will continue to be seen as vendors rather than partners.

The Road from Templating to Intelligence: What It Actually Takes

Genuine contextual personalization in BFSI is not a product you can buy from a vendor and deploy in a quarter. It is an organizational capability that must be built, and it requires changes at four levels.

Data Infrastructure

Real-time personalization requires real-time data. That means moving beyond nightly batch processing to streaming architectures – Apache Kafka, real-time feature stores, and event-driven decisioning pipelines. It means resolving the identity graph across channels so that a customer’s in-branch conversation, mobile app behavior, and contact center call are understood as part of a single coherent journey. This is expensive and time-consuming, which is why many banks are currently in the middle of multi-year cloud migration programs as a prerequisite.

Model Architecture

Rule engines need to be supplemented—not replaced—by machine learning models that can identify non-obvious behavioral patterns. Next Best Action (NBA) engines, pioneered at scale by firms like Pega and Salesforce, can process hundreds of contextual signals in real time to determine the most relevant intervention for each customer at each moment. The keyword is “supplement”. In a regulated industry, models need to be explainable, and human-readable rules remain essential for compliance.

Organizational Culture

The data science team can build the most sophisticated NBA engine in the world, but if the product team is still thinking in terms of “the home loan campaign” and “the credit card campaign,” the output will still be segment-driven. True personalization requires the organization to shift its mental model from campaigns, broadcast events aimed at groups, to journeys that are continuous, adaptive interactions with individuals.

Customer Trust and Consent

Perhaps the most underappreciated dimension. The more personal the personalization, the more important it is that customers understand how their data is being used and feel in control of it. Personalization that feels surveillance-like erodes the relationship it is meant to strengthen. GDPR and India’s DPDP Act are not obstacles to personalization; they are forcing functions toward a more transparent, consent-based approach that customers will ultimately trust more.

“The banks that will win the next decade are not those with the most data. They are those that can transform behavioral signals into genuinely helpful moments at speed, at scale, with consent.”

What Good Looks Like. Three Emerging Benchmarks

The good news is that the benchmarks for intelligent personalization in BFSI are becoming clearer. Three institutions stand out not for having solved the problem, but for having genuinely moved the needle.

DBS Bank (Singapore) has been widely recognized as one of the world’s most innovative banks, and its personalization strategy is a large part of why. DBS’s AI-driven insights engine, deployed across its mobile app in Singapore, India, and Indonesia, analyzes transaction patterns to generate proactive financial nudges. A customer whose grocery spend has increased 30% over three months might receive a suggestion to review their monthly budget. A customer who has been making EMI payments on time for 18 months might receive a pre-approved personal loan offer before they think to ask for one. DBS reported in its 2023 annual report that AI-personalized interactions drove a 20% higher product acceptance rate compared to generic outreach.

Bajaj Finserv (India) has made significant strides in using its Experia app to move from product-push to life-stage-aware engagement. Customers who have just taken a home loan are not immediately cross-sold a credit card. Instead, the system identifies that they are likely in a post-purchase consolidation phase and surfaces relevant content: home insurance comparisons, utility payment automation, and property tax reminders. The insight is simple but profound: the best time to sell the next product is not always now.

Conclusion. Intelligence Is Not Optional

Personalization has become one of the most overused words in financial services marketing. It appears in every strategy deck, every vendor pitch, every digital transformation roadmap. And yet, for most customers, the lived experience of financial services personalization remains generic at best and patronizing at worst.

The reason is not that the data does not exist. It does. The reason is not that the technology is unavailable. It is. The reason is that most BFSI organizations have confused the scaffolding of personalization such as CRM platforms, customer data platforms, marketing automation tools with personalization itself.

Real personalization is not about using someone’s first name. It is not about remembering their birthday. It is not about showing them products that their demographic segment statistically tends to buy. Real personalization is about understanding the specific, individual context of a specific human being at a specific moment and responding in a way that is genuinely useful, timely, and respectful of their autonomy.

That requires intelligence: computational intelligence to process signals at scale, organizational intelligence to act on them quickly, and emotional intelligence to know when to intervene and when to stay silent.

The institutions that crack this, and a small number are genuinely beginning to, will not just win market share. They will redefine what it means to have a relationship with a financial institution. They will transform a category that has been defined by transactions into one defined by trust. Personalization without intelligence is just templating. And in a world where customers have never had more choices, templating is no longer enough.

Sources:

McKinsey & Company – Next in Personalization 2021, 2023 Update. | Accenture – Banking Consumer Study 2023. | Salesforce — State of the Connected Customer, 5th Edition 2023. | DBS Bank – Annual Report 2023. I Forrester Research – The State of Digital Banking 2023. | Bajaj Finserv – Experia Product Documentation 2023. | HDFC Bank – echnology and Digital Transformation Report 2022–2023.

Post a Comment